In our example,we will stick to the Gordon Gorwth model as illustation. Based on the timing of cash flows, we cancalculate how long (in terms of year) they are from the valuation date. For theFY19 cash flow, we need to discount 0.5 year; For the FY20 cash flow, we need1.5 year and so on.

Why Would You Use a DCF Model?

It’s essential to use reasonable and well-founded assumptions when applying any of these methods to ensure the accuracy and reliability of the valuation. The technical definition of WACC is the required rate of return for the entire business given the risks to investors of investing in the business. Meanwhile, the layperson’s (and probably analyst’s) definition of WACC is the rate used to discount projected Free Cash Flows (FCF) in a DCF model.

What Happens When We Add the Terminal Value?

If you’d like to see how the terminus works in detail, with commentary, see the attached download. If these tests are failed, then it’s a good indication that the company has not reached a steady state yet. To do this, analysts use another formula referred to as the present value of a perpetuity. Julia Kagan is a financial/consumer journalist and former senior editor, personal finance, of Investopedia. Once it has done that, management should think about expanding the store count or pursuing debt-funded add-on acquisitions.

What is the Discounted Cash Flow Method?

However, the perpetuity growth rate implied using the terminal multiple method should always be calculated to check the validity of the terminal mutiple assumption. The terminal value (TV) captures the value of a business beyond the projection period in a DCF analysis, and is the present value of all subsequent cash flows. Depending on the circumstance, the terminal value can constitute approximately 75% of the value in a 5-year DCF and 50% of the value in a 10-year DCF. As a result, great attention must be paid to terminal value assumptions. So, to be more accurate in using cash flows to value a business, you’re going to need to discount the money to be received in the future.

- The Cost of Debt represents returns on the company’s Debt, mostly from interest, but also from the market value of the Debt changing.

- FCF (and Terminal Value, which uses FCF as an input) are the more sensitive.

- Moreover, year 4 cash flows are determined by year 3 cash flows, as that is the way the business works.

- Your goal is to calculate the value today—the present value—of this stream of future cash flows.

- The Exit Multiple DCF Terminal Value formula is used in the Discounted Cash Flow (DCF) valuation method to estimate the value of a business or investment at the end of a projected period.

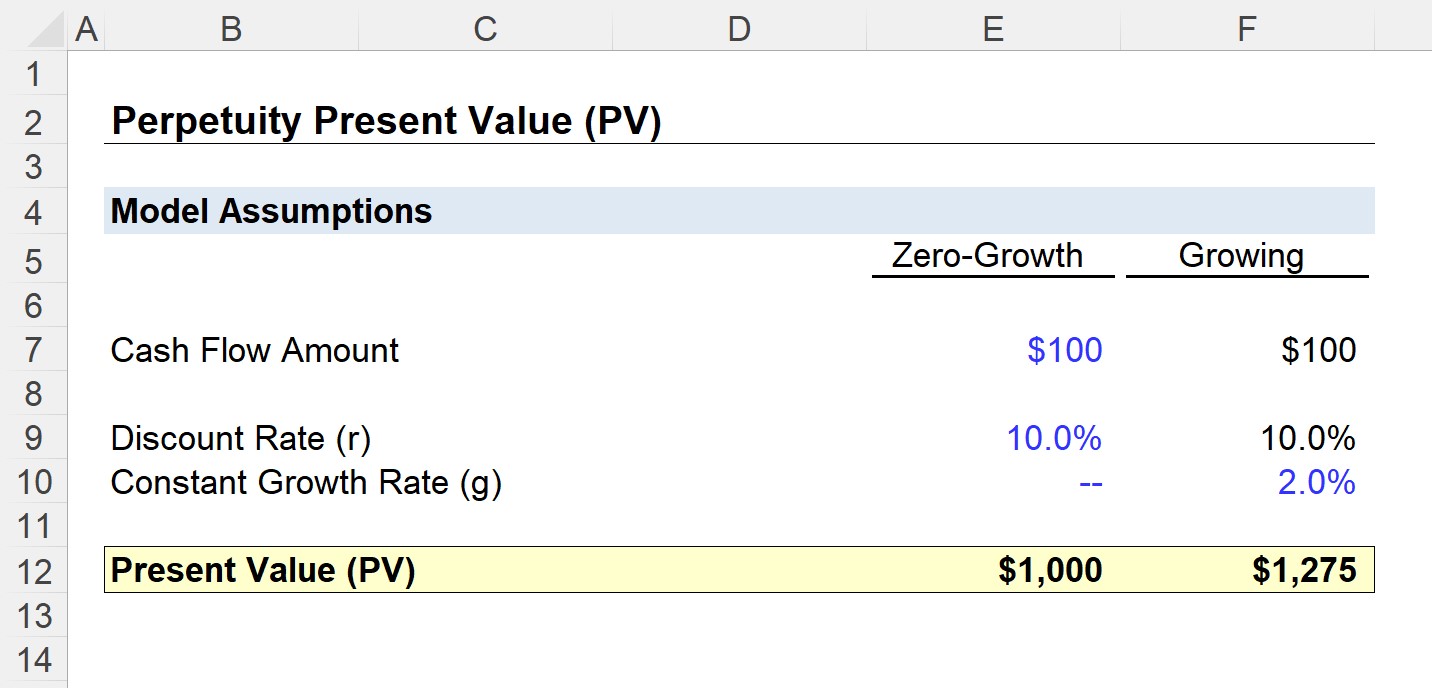

Although perpetuity is somewhat theoretical (can anything really last forever?), classic examples include businesses, real estate, and certain types of bonds. An analyst uses the finite present value of perpetuity to determine the exact value of a company if it continues to perform at the same rate. If you perform multiple valuations per year, and valuations are a significant part of the dcf perpetuity formula work you do, then using a tool that automates most of the process can make your life much easier. Otherwise, we hope the explanation above has helped you wrap your head around what a DCF analysis is, and how to use one. There are two methods, and one option is to combine them both and use the average. We had to calculate the Cost of Equity using the CAPM method as previously described.

Perpetuity in the financial system is a situation where a stream of cash flow payments continues indefinitely or is an annuity that has no end. In valuation analysis, perpetuities are used to find the present value of a company’s future projected cash flow stream and the company’s terminal value. Essentially, a perpetuity is a series of cash flows that keep paying out forever.

If not, you need to re-think your assumptions or extend the projections. No, you don’t know whether the Year 10 growth rate will be 10% or 8% or 12%, but you should have an idea of whether it will be closer to 10% or 20%. Therefore, if we had more time and resources, we might create a few operating scenarios, similar to the Uber and Snap models, to assess the results in “growth” vs. “stagnant” vs. “decline” cases. And Levered Beta tells you how volatile this stock is relative to the market as a whole, factoring in both business risk and risk from leverage (Debt). The Equity Risk Premium (ERP) is the percentage the stock market is expected to return each year, on average, above the yield on these “safe” government bonds.

The terminal value is calculated in the terminal year and we will discuss more on how to do terminal value calculation later in this article. Also, the DCF approach values a business at a single point in time (i.e., the Valuation Date). So the very first step is to determine the Valuation Date of your DCF. The Expected Inflation Rate should be inflation expectations for the Terminal Period (into perpetuity). The Expected Inflation Rate is for the currency in which the valuation is conducted. Generally, the Risk-Free Rate assumed should incorporate the Expected Inflation for the Terminal Period.

Leave a Reply